Digitalization affects financial sector and opens new possibilities for banks and other companies. What are the new innovations in banking and how they impact different financial services?

Financial Services Sectors

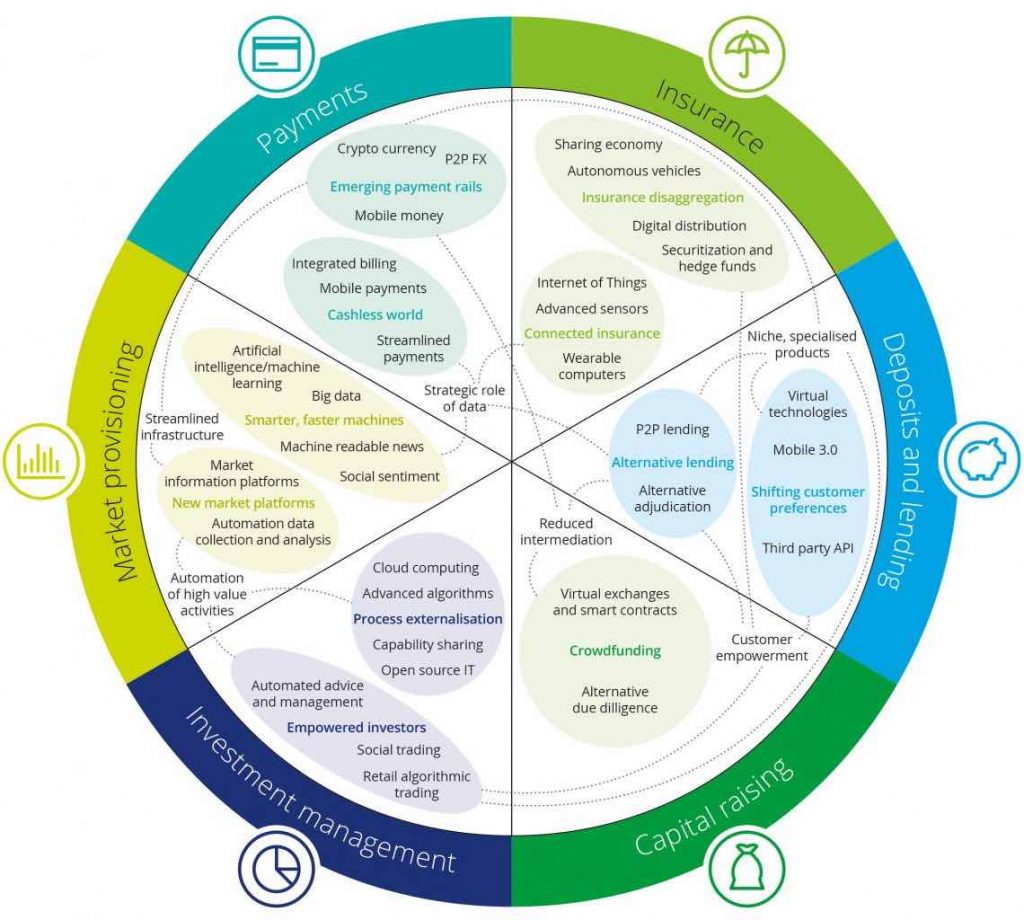

Financial services can be roughly divided to 6 business sectors, as seen below in the chart:

This chart is compiled by Deloitte and I think it summarises quite well the financial services landscape and how new innovations are impacting the market.

{kind=link}

Payments

Everyone has already seen how payments have become cashless and ever more mobile. Internet companies have already competing with tradional banks in providing mobile and online payment solutions to consumers and businesses. Android Pay, Apple Pay, Alipay, WeChat and Amazon Pay are the most visible services. Also tradiotional banks have introduced similar services, like LyfPay in France, Siirto in Finland, and PayByBankApp in the UK. Some of these systems provide real-time money transfer from account to account and some work more like credit card or mobile wallet.

Next innovation is digital money, Bitcoin being the most well known example. It cannot be yet said what and how will digital currencies (or crypto currencies) to be used by public, or will they ever. But what is certain is that there will be more pilots and options available.

Insurance

Insurance industry is innovating with new services that offer better tailoring for customer needs and expanding to offer new type of services outside traditional insurance contacts.

Sharing economy opens possibilities to offer new services, such as mobility-as-a-service (MaaS). Customer buys service and does not need to own the physical infrastructure (such as cars or bicycles). Insurance is just part of the service. Another example is Internet of things (IoT) services that can be used to offer and get better data used with insurances. For example, IoT sensors can be placed inside structures of a house and help to monitor leaks and moisture. This benefits both the insurer and the customer.

Investments and Market Provisioning

This is very much about market & transactional data and automating processes. Investment management and especially trading has been very automatic for quite some time already and that trend will continue. There is more and more data available for algorithms and artificial intelligence is part of this evolution. Market analysis is faster and there are more data points available in real time.

With more automation and data, companies can offer new market places and offer new types of assets for market and for wider audience. Some assets can also become much more liquid when they are digitalised and sales processes are made digital (this may include real estate, for example).

Lending and Capital Raising

Lending and capital raising can be organised in a new way using digital platforms. Customers can lend money to other customers via peer-to-peer (P2P) lending services. Crowdfunding has been made popular for new projects & startups by Kickstarter and Indiegogo. There are already big services for P2P consumer lending, such as US-based LendingClub. Multiple independent market places in many countries are raising capital for startups and SMEs, such as Invesdor.com.

Also tradional financial services and banks have established their own “market places” for their customers. A bank can offer hand-picked companies for their customers and customers can diversify his or hers portfolio with shares of private small companies. For example, Finnish Nordea Bank has launched own crowdfunding service.

Customer data

I am adding one segment that is not in the chart because I think its importance will increase. I am talking about personal customer data. That includes behavioural data, transactional data (what am I buying and when), and it can be combined with historical data and even with social media data.

My own data will be valuable to financial services, for example. This means that some of the services that are now premium services might become completely costless for consumer if I open my data to service providers. Data usage and privacy issues will become more prominent than ever before. EU has already made new regulation for handling of customer data, GDPR regulation. As a customer, I can only hope that also other countries will take data privacy seriously.

On the other hand, banks should give me a possibility to move and use my data to other digital services. PSD2 regulation in the EU is forcing banks to open account data and account payment interfaces to 3rd party services. This will empower consumer and will make competition tougher because customer can change provider easily and also use different service providers at the same time.

What Does All This Mean?

As a customer, I should get better tailored financial services and products. Because of automation and competition basic banking costs should go down. On the other hand, controlling my date will be more important that before – it is basically an asset I can sell. This is totally new to many consumers and will have impact on the service lanscape, as well. New technologies can actually give more power to consumer.

Banks and other financial services will face new competition (like Google and Amazon) and they will have to open their data and this means they have to rethink their business position and value chain. But it also opens new product and services opportunities and possibly new revenue streams. As a company, I can offer better services and help my customers more automatically in the right context and with perfect timing.

Read More

Palkkaus.fi yrityksille ja yhteisöille (in Finnish)

Palkkaus.fi tilitoimistoille (in Finnish)